The Agentic Future: All Memory Is Equal, Except Some Memory Is More Equal Than Others

George Orwell suggested that control of the record is control of reality. AI now faces the same question: who owns, edits and monetises memory may own the next infrastructure bottleneck

This Crypto AI & Robotics newsletter consists of three key parts:

Snippet Partner: Naoris Protocol

Theme of the Week: AI Memory Trade

Landscape Analysis: Micron, SKHynix, Samsung, Broadcom, Astera, Rambus, Walrus, Filecoin, Arweave, Hippius

If you have any questions feel free to reach out to me on X or message my business X account ‘Khala Research’

The quantum mandate skipped the networks holding your money

Two new US executive orders just put quantum computing on a clock:

One targets a cryptographically-relevant quantum computer by 2028

The other moves federal critical infrastructure onto post-quantum cryptography by 2030 and 2031, a timeline pulled forward four years

NSA, CISA, DHS and Commerce are all named, with “harvest now, decrypt later” cited as the threat. But the orders cover government systems and stop there. That leaves the decentralized networks holding most onchain assets with no deadline and no protection.

This is the gap Naoris Protocol was built to close. It is a native post-quantum Layer 1, secured by NIST-standard cryptography from genesis rather than retrofitted later, with mainnet live since April.

The government is still racing to mandate quantum-resistant infrastructure. Naoris already runs it for the chains the orders leave out.

This newsletter goes out weekly to 7.2k+ subscribers.

Please don’t hesitate to message me directly for sponsorship or partnership enquiries.

All Memory Is Equal, Except Some Memory Is More Equal Than Others

George Orwell spent two books warning that whoever controls the record controls everything that follows, including memories.

In Animal Farm, the commandments change on the barn wall while the animals are told nothing has changed:

In 1984, the past is edited until the present becomes impossible to challenge:

He was writing about politics, language and power… but the warning now applies to AI infrastructure, and in particular, memory.

The next phase of AI will be shaped by memory: who owns it, who can access it, who can edit it, who can revoke it, and who gets paid when it becomes scarce.

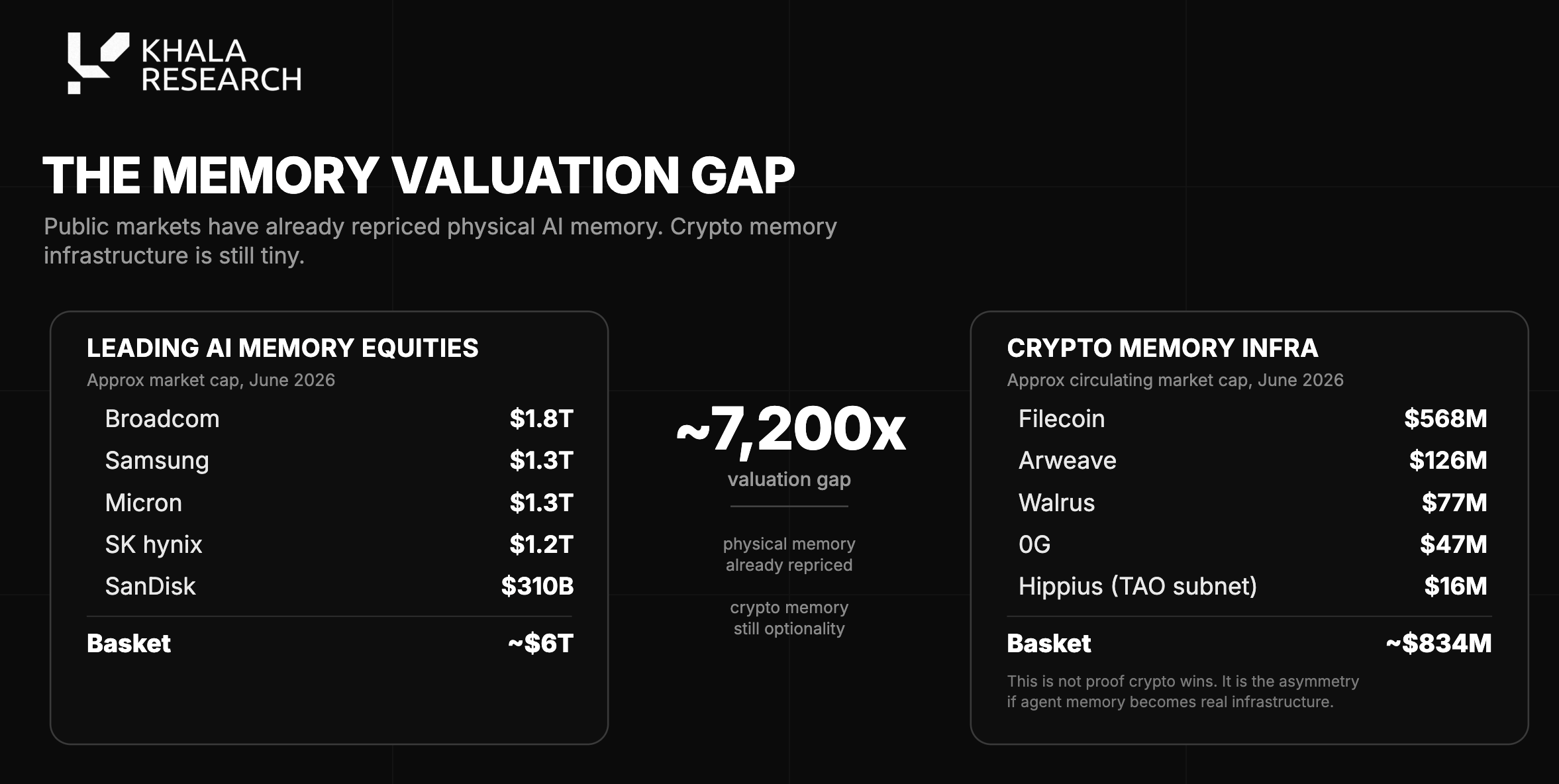

The market has already repriced the physical side of this trade through HBM, DRAM, NAND, interconnects and storage.

Crypto is still pricing the agent-memory side as if it were generic storage or early middleware.

The first phase of AI was compute; the second phase was power; the third phase is memory, and memory is where the trade becomes more interesting.

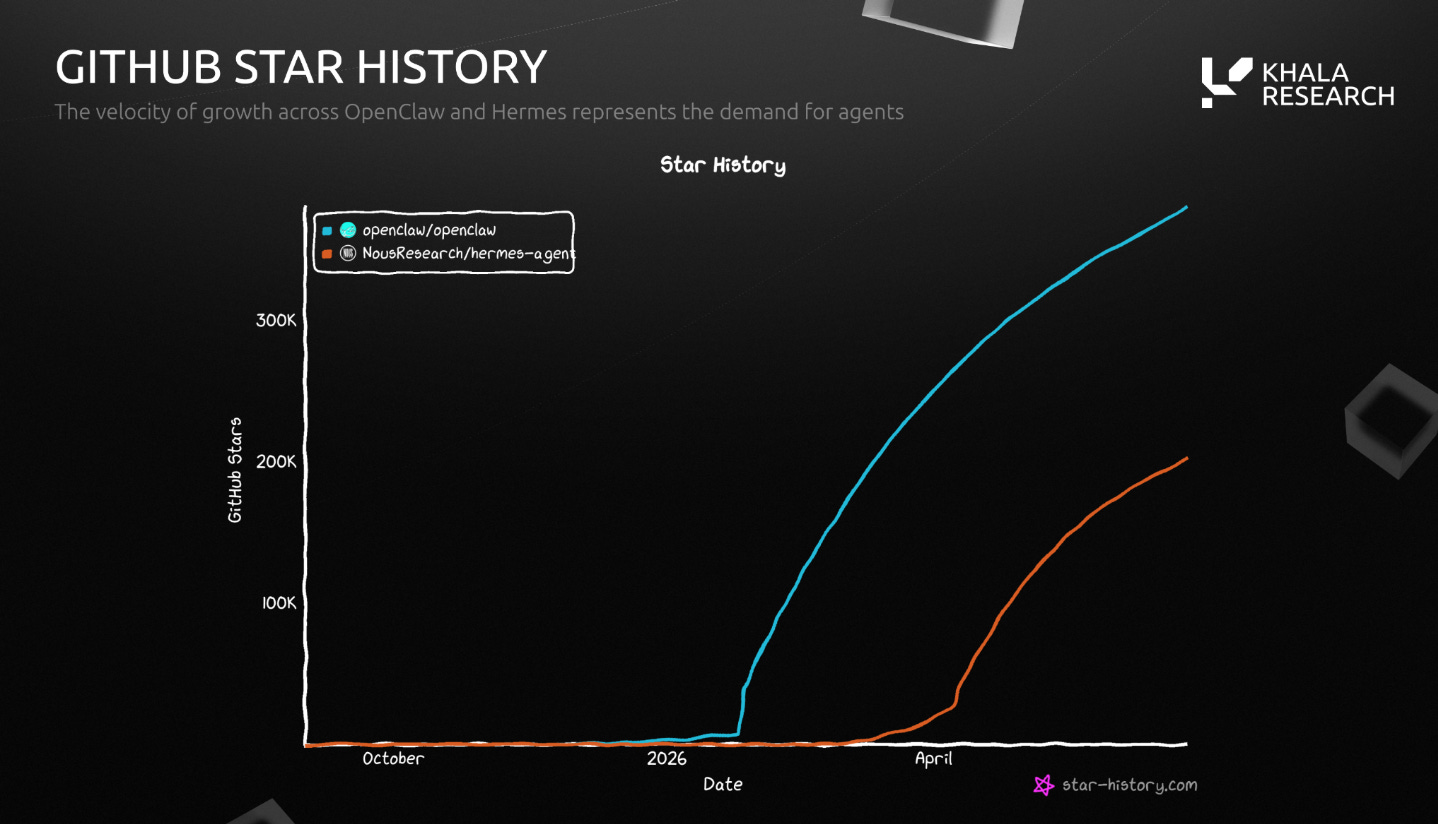

If agents become a major interface for the internet, memory becomes their past, their permission system and their operating state; particularly as trillions of agents come “alive”, which we are seeing through protocols like Hermes and OpenClaw:

That makes the memory layer one of the most important markets in AI.

“All memory is equal, except some memory is more equal than others”

1. The commandment on the barn wall

The AI market still talks too much about compute. Compute matters, but AI systems also need memory capacity, memory bandwidth and memory movement.

A GPU with constrained memory cannot run large workloads efficiently.

A model without persistent state forgets the user.

An agent without memory becomes a repeated prompt loop.

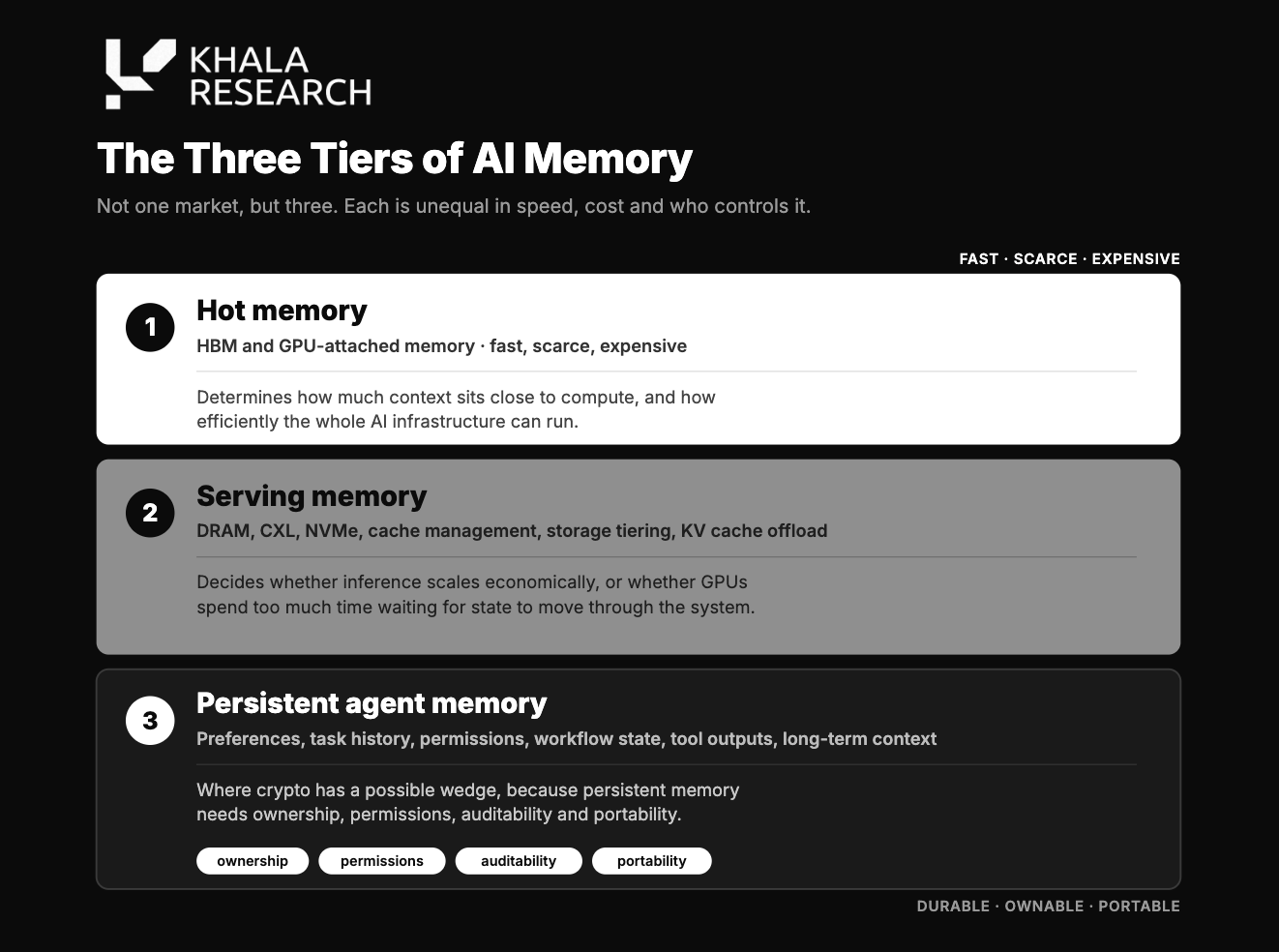

Memory now matters in three layers:

The first is hot memory: HBM and GPU-attached memory. It is fast, scarce and expensive. It determines how much context can sit close to compute and how efficiently AI infrastructure can run.

The second is serving memory: DRAM, CXL, NVMe, cache management, storage tiering and KV cache offload. This layer decides whether inference can scale economically or whether GPUs spend too much time waiting for state to move through the system.

The third is persistent agent memory: user preferences, task history, permissions, workflow state, tool outputs and long-term context. This is where crypto has a possible wedge, because persistent memory needs ownership, permissions, auditability and portability.

The Orwellian tension provides clarity: The same memory that makes agents useful, also makes them risky.

A useful agent remembers your preferences, research, accounts, workflows and decisions.

A dangerous memory layer stores those details inside a closed platform where the user cannot see the full record, cannot move it easily and cannot verify how it changes.

The AI version of “Big Brother is watching you” is less obvious than a camera surveillance network.

It’s an agent that remembers everything while the user cannot see where that memory lives, who can access it, or what has been rewritten over time.

2. Some memory is more equal than others

The public market has already identified the first side of the trade.

HBM, DRAM, NAND, controllers, interconnects and storage systems have moved to the centre of the AI capex cycle. Memory is no longer viewed only as a cyclical hardware category. In AI, memory is a strategic constraint.

The rationale is simple: AI consumes memory bandwidth, memory capacity and memory movement. Longer context windows need more memory; more inference users need more memory; more agents need more memory; more tool calls need more state; more concurrency multiplies the whole problem:

The GPU trade was always a system trade; the system includes compute, memory, networking and power. If memory is constrained, the system is constrained.

This is why NVIDIA’s H200 matters as a memory product as much as a compute product. The most valuable real estate in AI infrastructure is measured in memory capacity and bandwidth because that is what determines how much work can be kept close to compute.

The commandment on the barn wall would read:

“Compute attached to scarce memory is more valuable than compute alone”

3. The Inner Party owns the fast tier

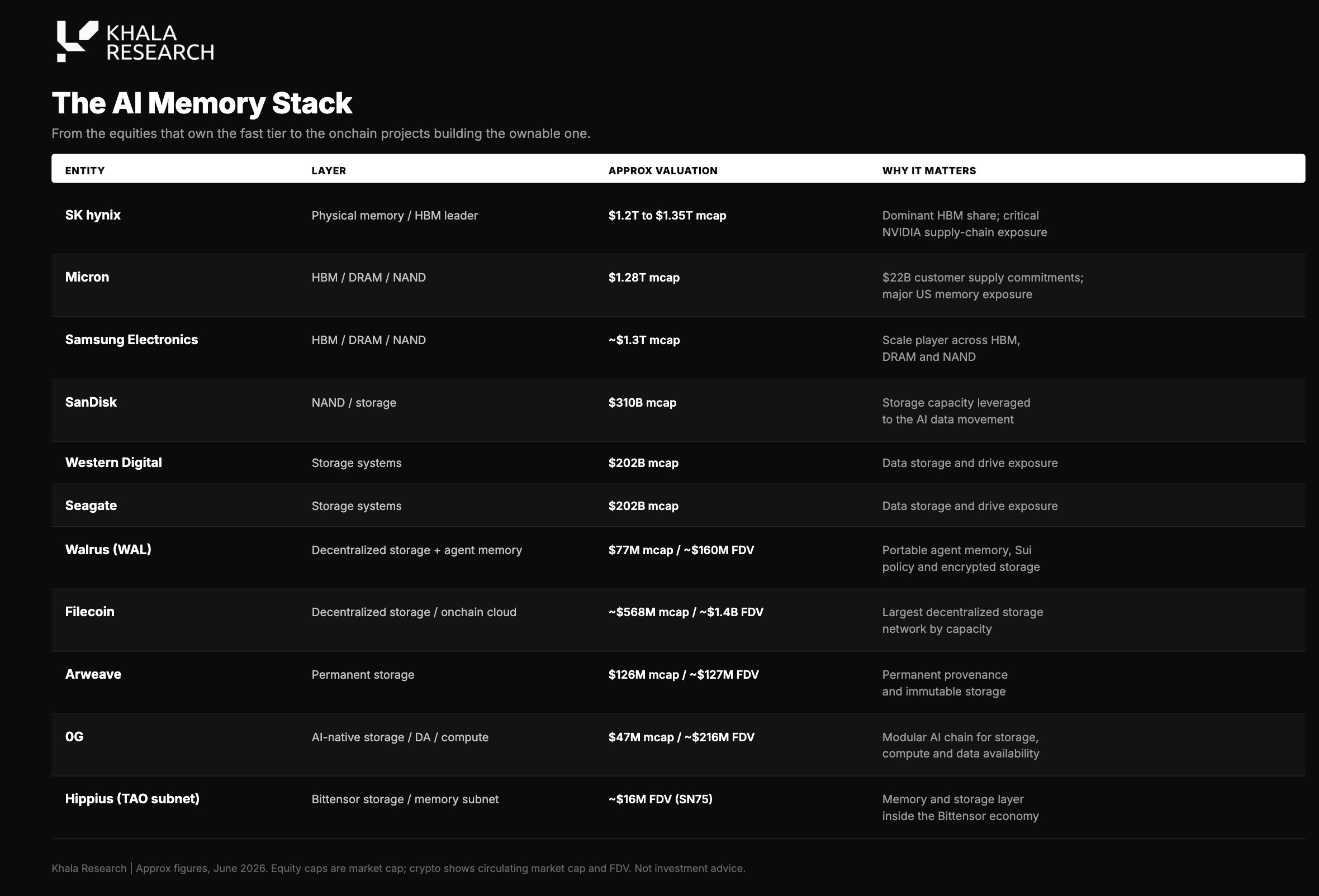

The physical memory trade is already a large public-market theme.

Micron, SK hynix and Samsung are direct expressions of the AI memory buildout.

Astera Labs, Rambus, Western Digital, Seagate and SanDisk sit in the broader memory, interface and storage stack.

The best way to read this part of the market is through scarcity.

HBM is difficult to manufacture, closely tied to advanced packaging and reserved by the largest AI customers.

DRAM and NAND benefit from the same demand wave, although with different degrees of pricing power.

Interconnect and memory-interface companies benefit from the rising complexity of moving state through the system.

This is the Inner Party of the memory stack: the companies closest to the fastest and most constrained memory tiers:

i) Micron

Ticker: MU

Approx valuation: $1.3T

Layer: HBM, DRAM, NAND

Memory role: US pure-play memory torque

Micron is one of the cleanest public-market memory trades because it gives direct exposure to HBM, DRAM and NAND.

The company used to be treated as a cyclical DRAM business.

“DRAM is probably going to be 30 to 40% of all hyperscaler CapEx next year, every hundreds of billions of dollars spent goes straight to DRAM" - (Gavin Baker, CIO of Atreides Management)

Although the AI cycle has changed that perception because memory supply is now a strategic input for data-centre customers.

Customer behaviour changes when memory becomes scarce:

In a normal memory cycle, buyers wait for price weakness.

In an AI infrastructure cycle, buyers reserve supply because short memory means short inference capacity.

Micron’s recent multi-year supply commitments are evidence that customers want guaranteed access rather than spot exposure to a volatile market.

The bull case is continued HBM growth, tight DRAM and NAND supply, and stronger pricing for longer than the market expects.

The bear case is the old memory cycle returning. If capacity catches up too quickly, the market will move from “memory is strategic” back toward “memory is oversupplied”.

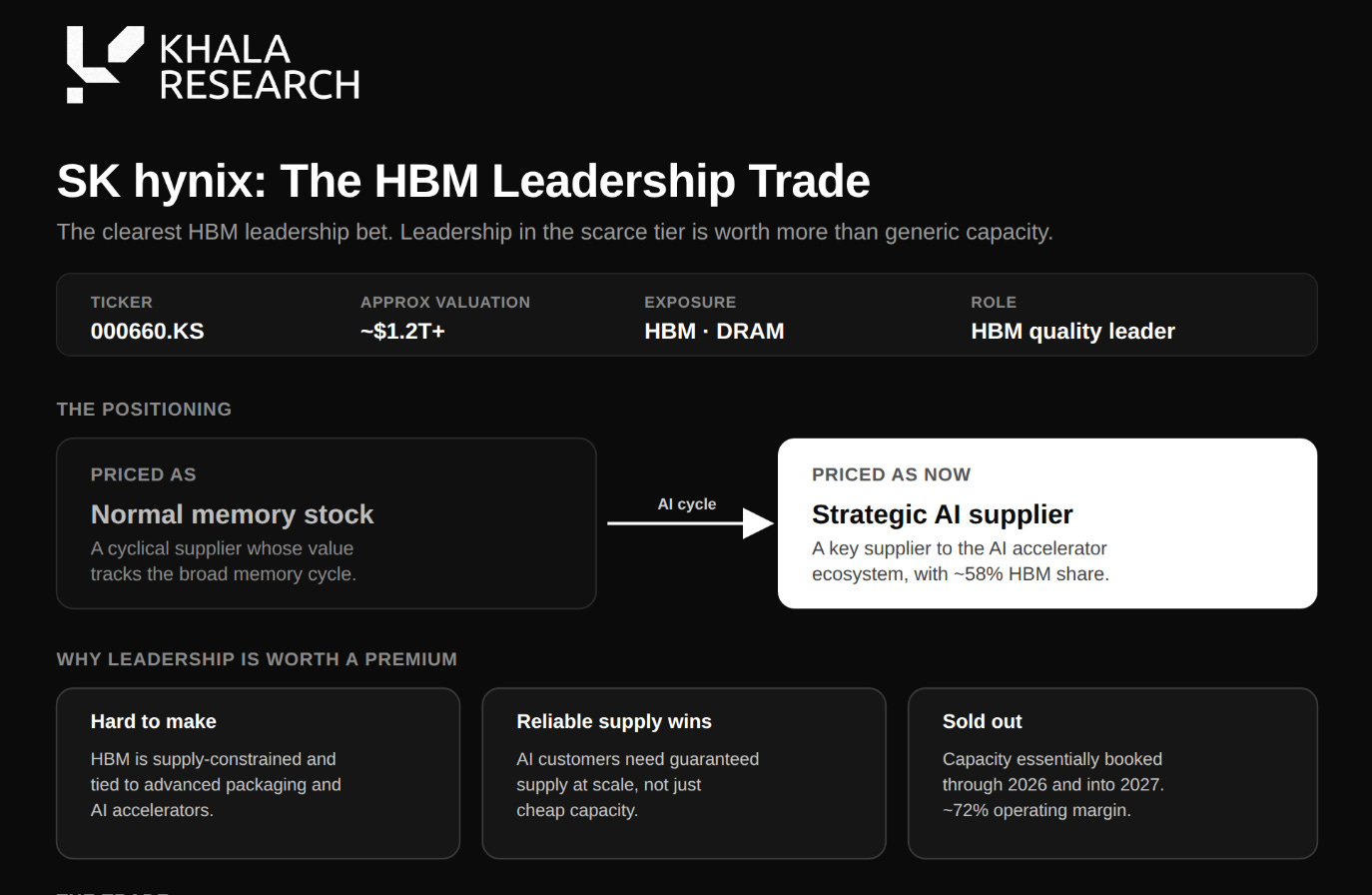

ii) SK hynix

Ticker: 000660.KS

Approx valuation: $1.2T+

Layer: HBM, DRAM

Memory role: HBM quality leader

SK hynix is the clearest HBM leadership trade.

HBM is difficult to manufacture, supply-constrained and closely tied to advanced AI accelerators. Leadership in this category is worth more than generic memory capacity because AI customers need reliable supply at scale.

The company has become one of the key suppliers for the AI accelerator ecosystem. That gives it strategic value in the current cycle and explains why the market treats it as more than a normal memory stock.

The bull case is continued HBM leadership, premium pricing and long-duration supply agreements, oh and a Nasdaq listing?

The bear case is competition. Samsung and Micron are investing heavily, and in memory markets high margins always attract new capacity

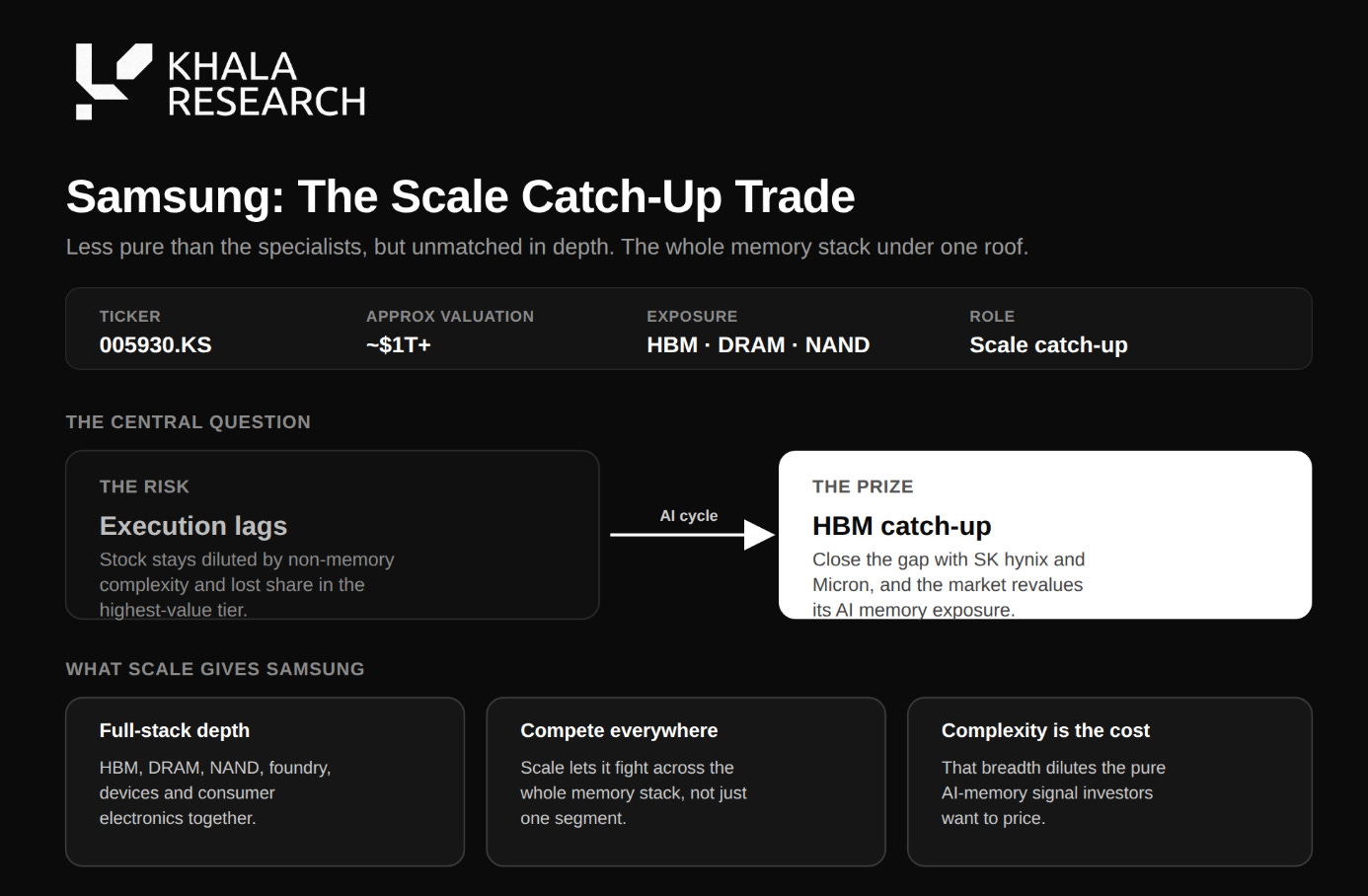

iii) Samsung Electronics

Ticker: 005930.KS

Approx valuation: $1T+

Layer: HBM, DRAM, NAND, foundry, devices

Memory role: Scale catch-up

Samsung is less pure than Micron or SK hynix, but its scale matters. It has depth across HBM, DRAM, NAND, foundry, devices and consumer electronics. That makes the stock more complex, but it also gives Samsung the ability to compete across the whole memory stack.

The key question is HBM execution. If Samsung closes the gap with SK hynix and Micron, the market can revalue its AI memory exposure. If execution lags, the stock remains diluted by non-memory complexity and by the loss of share in the highest-value part of the cycle.

The bull case is a successful HBM catch-up combined with strong DRAM and NAND demand.

The bear case is timing. In AI memory, customers commit to suppliers that can deliver now, and delays can cost years of share.

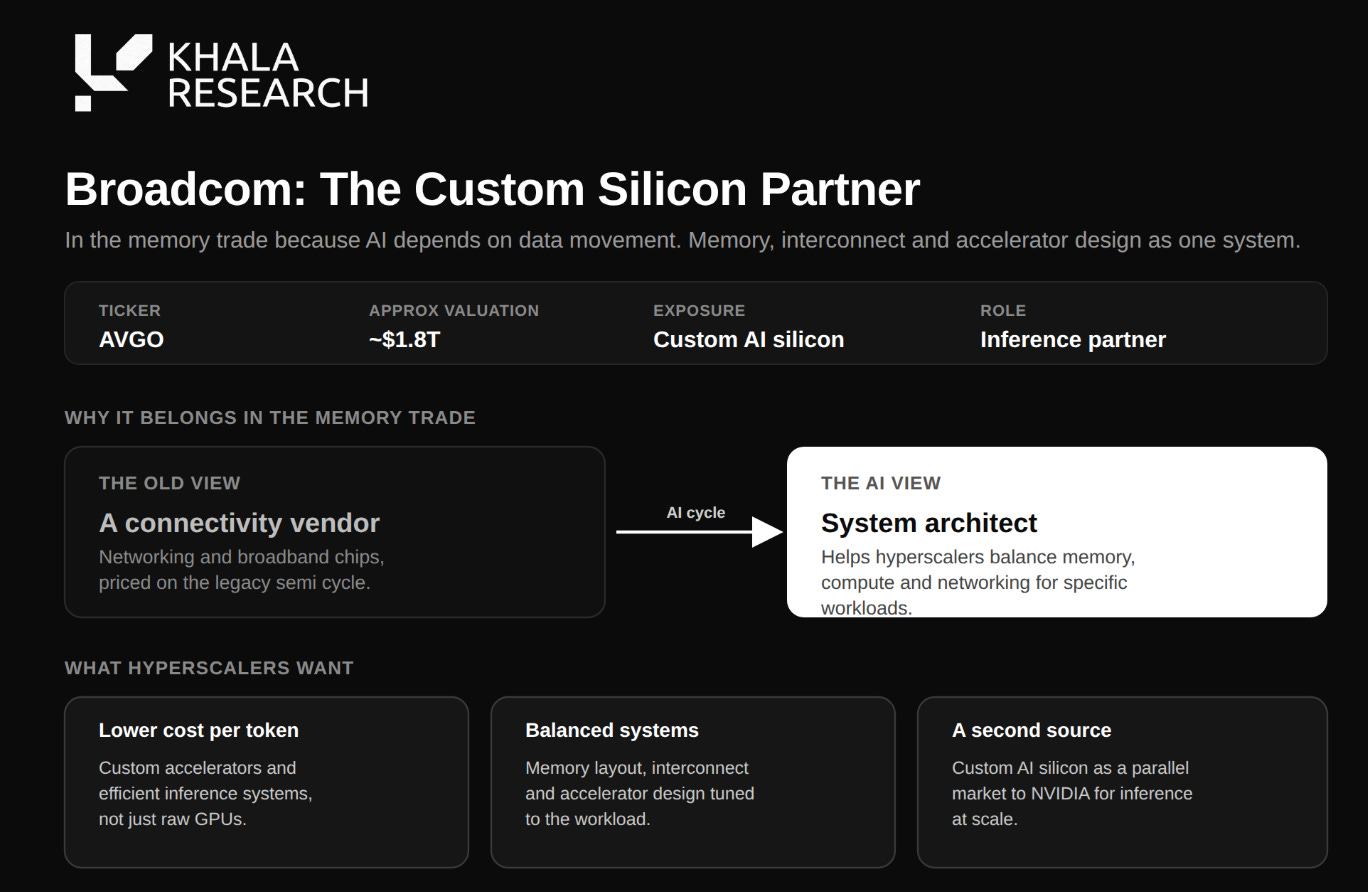

iv) Broadcom

Ticker: AVGO

Approx valuation: $1.8T

Layer: Custom AI silicon, networking, ASICs

Memory role: Custom inference system partner

Broadcom belongs in the memory trade because AI infrastructure depends on data movement. Hyperscalers want lower cost per token, better networking, custom accelerators and more efficient inference systems. Memory layout, interconnect and accelerator design are central to that equation.

Broadcom benefits if custom AI silicon becomes a parallel market to NVIDIA for inference at scale. Its role is less about owning HBM supply and more about helping the largest customers build systems where memory, compute and networking are balanced for specific workloads.

The bull case is continued growth in custom AI accelerators and networking.

The bear case is customer concentration, because a small number of large buyers can create huge revenue while also pressuring margins

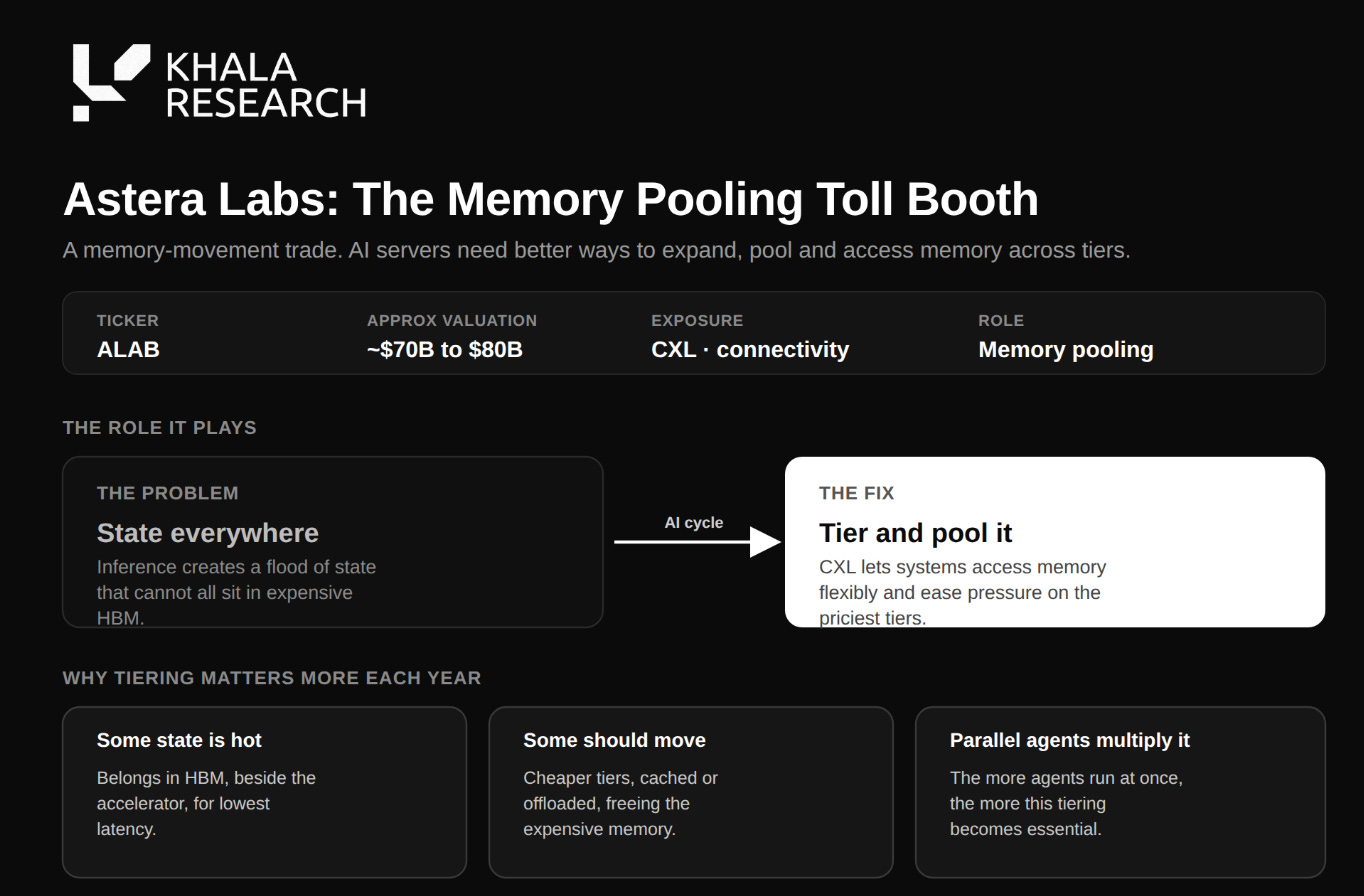

v) Astera Labs

Ticker: ALAB

Approx valuation: $70B to $80B

Layer: AI connectivity, CXL, memory expansion

Memory role: Memory pooling toll booth

Astera Labs is a memory movement trade. AI servers need better ways to expand, pool and access memory. CXL is one of the key technologies for this shift because it can help systems access memory more flexibly and reduce pressure on the most expensive tiers.

This matters because inference creates a lot of state. Some state belongs in HBM. Some should move to cheaper tiers. Some should be reused, cached or offloaded. The more agents run in parallel, the more important this tiering becomes.

The bull case is broad CXL adoption in AI servers.

The bear case is valuation; the market already gives Astera significant credit for future AI infrastructure growth

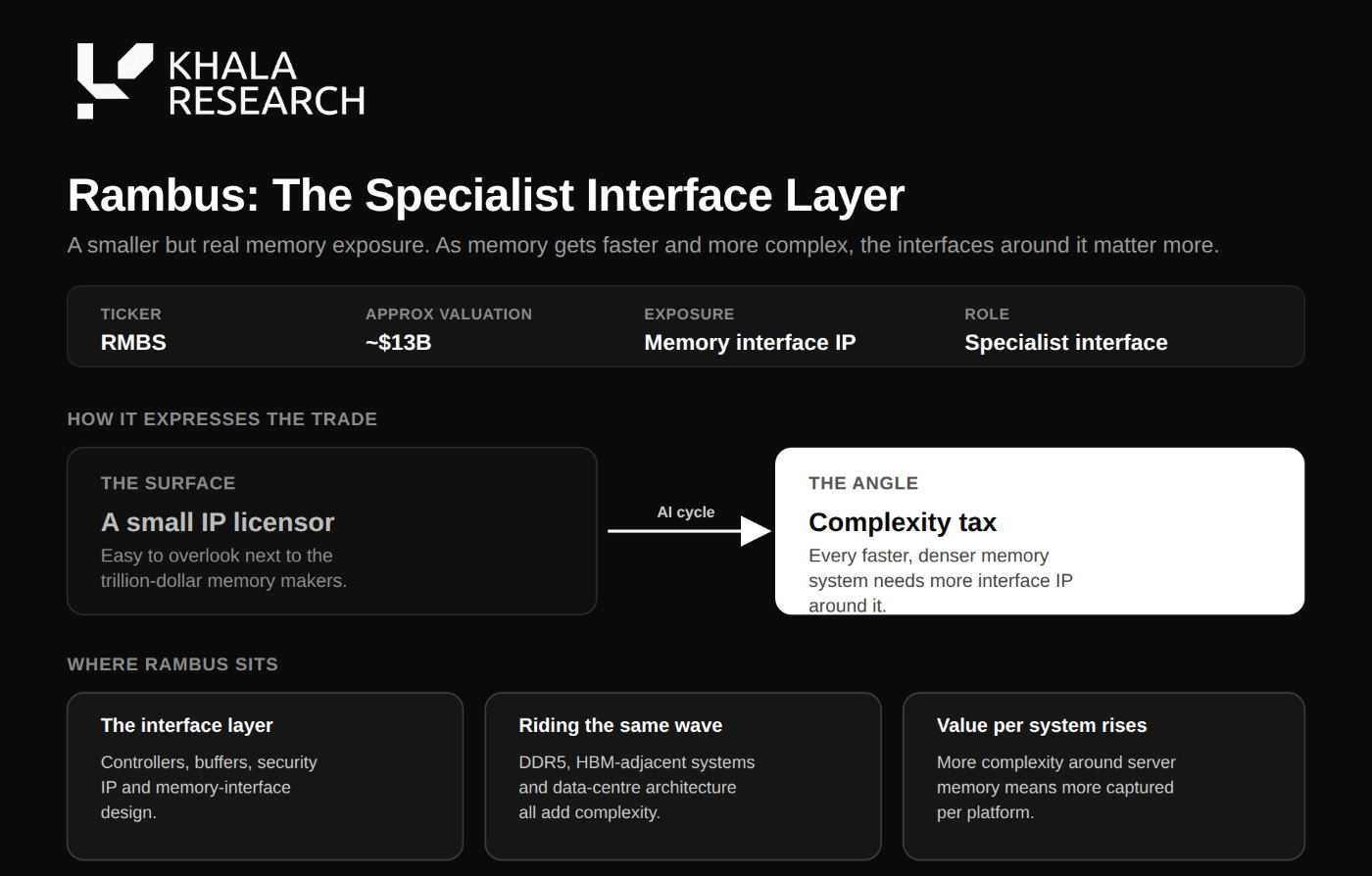

vi) Rambus

Ticker: RMBS

Approx valuation: $13B

Layer: Memory interface chips and IP

Memory role: Specialist interface layer

Rambus is a smaller but relevant memory exposure. As memory systems become faster and more complex, the interfaces around them become more important. Controllers, buffers, security IP and memory-interface design help the system function.

This is a less obvious way to express the trade, but it is still part of the same direction. AI infrastructure is creating more complexity around server memory, DDR5, HBM-adjacent systems and data-centre architecture.

The bull case is that memory complexity keeps rising and Rambus captures more value from interface IP and chips.

The bear case is that it remains a specialist supplier rather than a broad AI infrastructure winner

vii) SanDisk, Western Digital and Seagate

Tickers: SNDK, WDC, STX

Approx valuations: SanDisk $300B+, Western Digital $200B+, Seagate $200B+

Layer: NAND, SSDs, HDDs, storage systems

Memory role: Cold-memory beta

AI does not keep all memory beside the GPU. A large amount of AI data sits in colder storage layers: datasets, logs, embeddings, model checkpoints, videos, synthetic data, agent records and archives.

SanDisk, Western Digital and Seagate provide exposure to this cold-memory layer. This part of the trade is less scarce than HBM, but AI data growth still creates a major demand tailwind. The value is volume rather than premium scarcity.

The bull case is that AI turns storage into a structural growth market.

The bear case is commoditisation.

HBM has stronger pricing power because it is closer to the bottleneck. Storage gets the demand growth, but margins depend on whether the market avoids oversupply.

4. The Ministry of Truth runs inference

The memory bottleneck is not only about capacity and speed. It is also about whether the record can be trusted.

In Nineteen Eighty-Four, Winston Smith works at the Ministry of Truth rewriting records so the past always agrees with the present.

That is a useful frame for AI memory because a badly designed memory layer can produce a similar effect without a political villain. It can store the wrong thing, retrieve it as truth and carry that error forward across future decisions.

This is the harder product problem; a larger context window does not automatically create better memory. It can simply give the system more room to preserve confusion.

Persistent memory is valuable only if it can distinguish preference from fact, stale information from current information, permission from habit and correction from contradiction.

The risk is especially serious in agentic systems. An agent acts, pays, trades, files, books, moves data and writes to other systems. If its memory becomes corrupted, the error becomes operational. The agent may repeat a mistaken assumption, preserve outdated permissions, trust stale context or carry the wrong state into a real workflow.

Orwell had a word for holding contradictions in the mind and accepting both. He called it “doublethink”. In AI, the software version is a memory system that stores an error, retrieves it confidently and uses it to justify the next action becomes a huge risk with a plethora of hallucinations.

This is why the memory trade expands beyond hardware. The winners will not only store more state. They will help decide which state is true, which state is stale, who wrote it, who can change it and when it should be forgotten.

“A memory you cannot correct is a memory that controls you”

We should also pay attention to those who control the memory; they’ve been fined for price fixing previously:

5. Four legs good, two legs better

The most useful crypto angle is not faster memory. Crypto will not compete with HBM on latency. The crypto opportunity is persistent, permissioned, portable and verifiable memory for agents.

In Animal Farm, the original slogan:

“four legs good, two legs bad”

…gradually becomes:

“four legs good, two legs better.”

The animals do not experience one dramatic lie, but they experience a slow rewrite of the record by whoever controls the wall.

Agent memory has the same risk.

Today, most memory lives inside whichever platform created the agent. Your preferences, work context, wallet permissions, workflows and past interactions sit in a company’s store, in a format you may not control, under rules you did not write. If memory is the agent’s operating state, then control over memory becomes control over the relationship.

This is where crypto becomes relevant; the agent needs a record that cannot be silently edited by a platform, a history that proves who wrote each entry and when, and an access layer that lets the user grant, delegate and revoke permissions. Portability, signatures, audit trails, programmable access and user-owned records are crypto-native primitives.

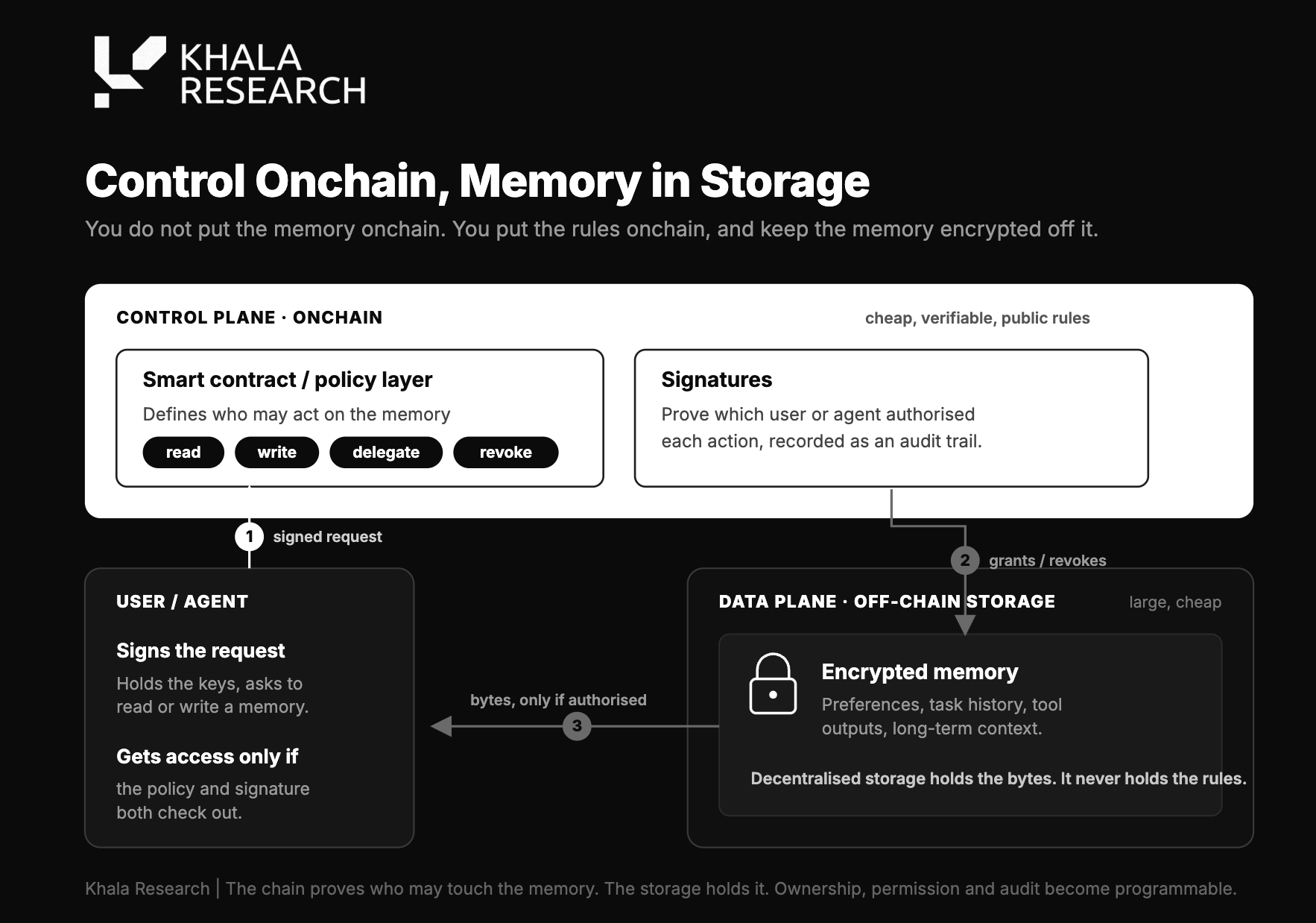

The point is not to put every memory onchain… that would be slow, expensive and unnecessary. The useful design is to put control onchain while the memory itself stays encrypted in storage:

A smart contract or policy layer can define who may read, write, delegate or revoke access, while signatures prove which user or agent authorised the action.

That is the crypto memory wedge: own the rules around memory rather than pretending to replace HBM.

6. The open memory layer

Crypto memory is earlier, smaller and less proven than the public equity memory trade. That is exactly why the category is interesting.

The physical memory trade has revenue, customer commitments, supply constraints and strategic urgency

The crypto memory trade has optionality, weak revenue, immature products and much smaller valuations. The opportunity is real only if agents turn memory into a workflow dependency

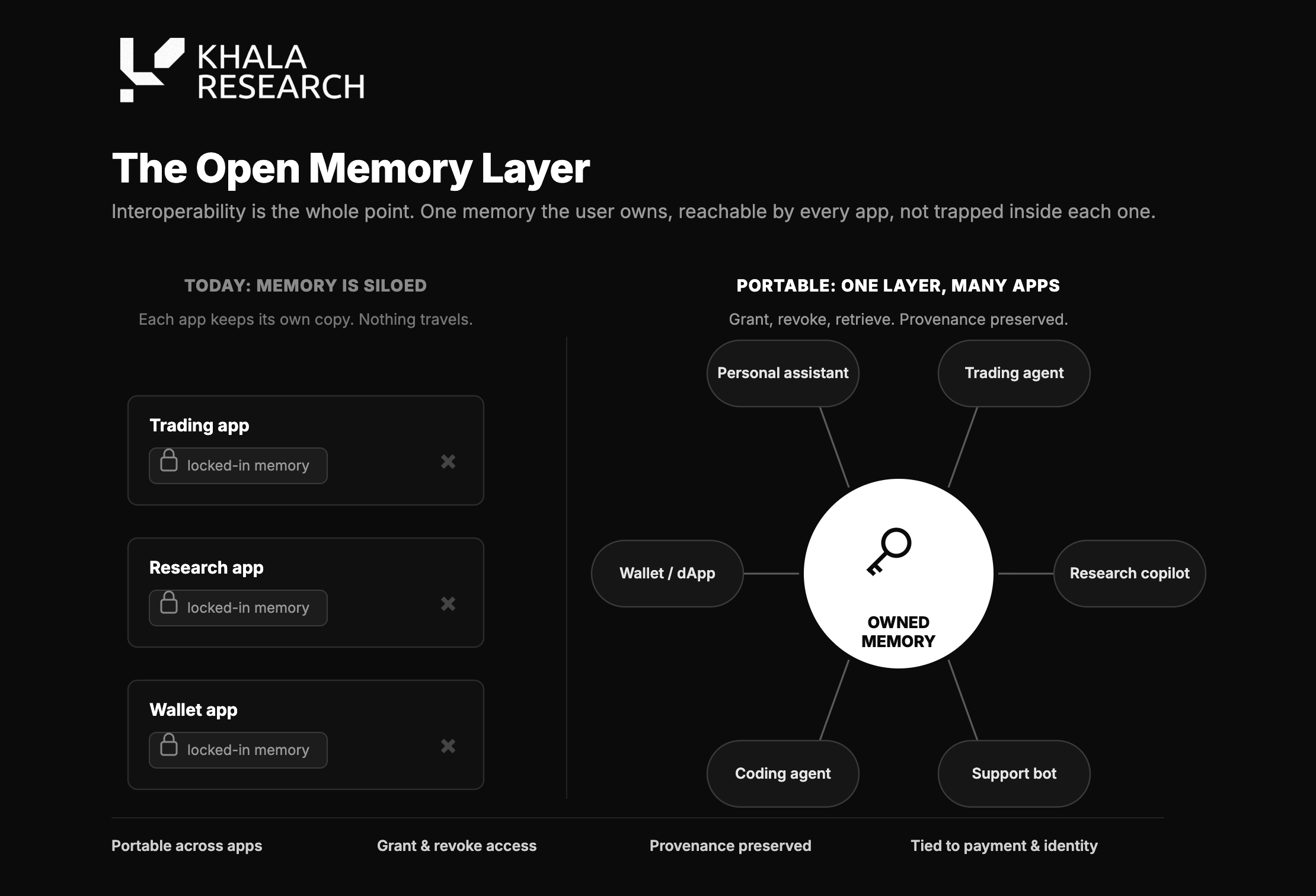

The strongest crypto projects will solve specific problems, making memory portable across applications… interoperability is supposed to be a core feature after all!

They will let a user or enterprise grant and revoke access, preserving provenance. They will support retrieval and will connect memory to payment and identity creating usage sinks tied to actual agent activity

Here are several protocols holding the memory baton in crypto:

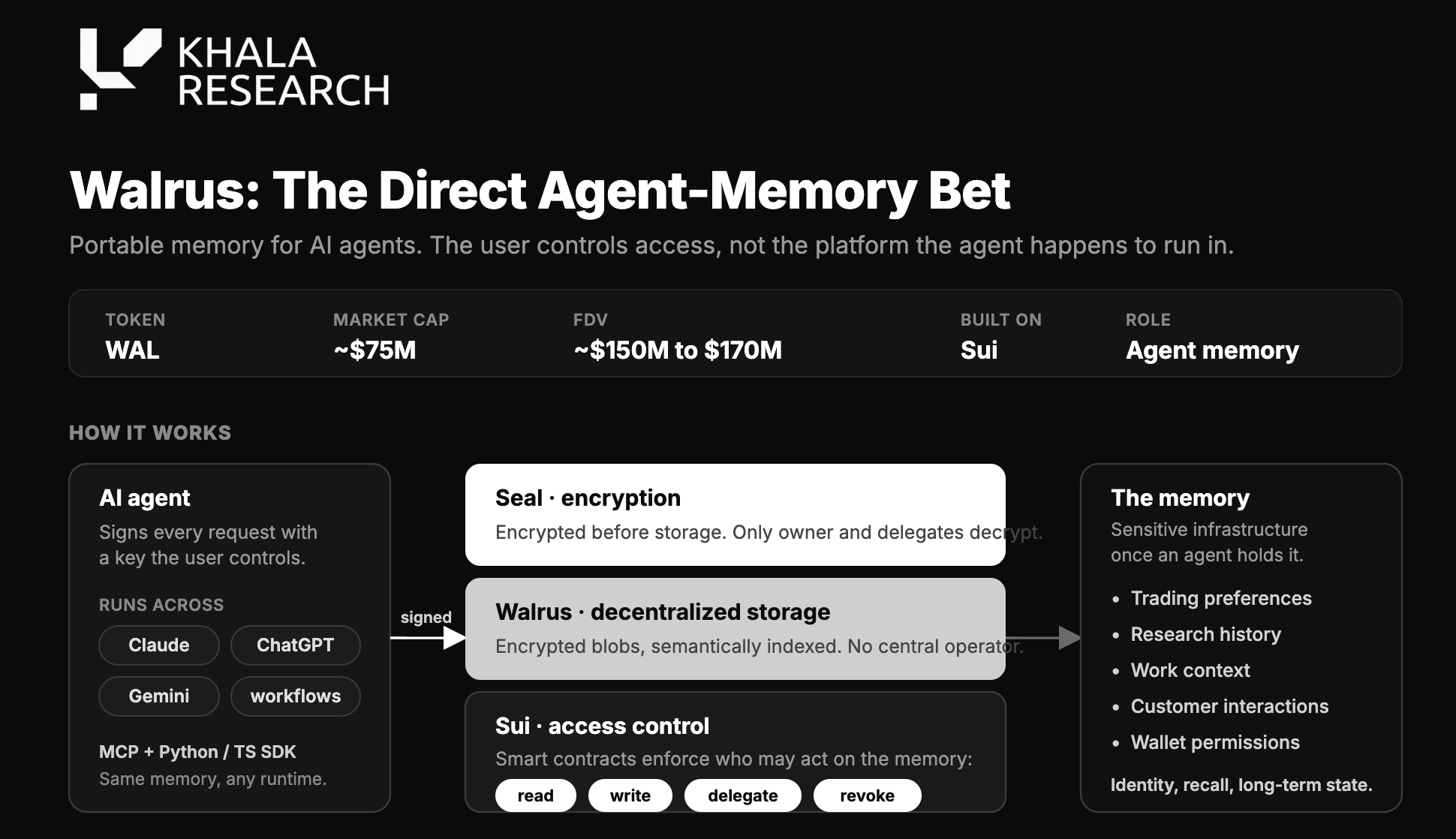

i) Walrus

Token: WAL

Approx valuation: $75M market cap / $150M to $170M FDV

Layer: Decentralized storage and portable agent memory

Memory role: Direct agent-memory bet

Walrus is the cleanest direct crypto memory project because it explicitly targets portable memory for AI agents:

The core idea is straightforward: agents should be able to carry memory across applications and providers while access is controlled by the user, builder or agent rather than by one platform.

This matters because agent memory includes identity, permissioning, recall and long-term state. If an agent remembers trading preferences, research history, work context, customer interactions or wallet permissions, that memory becomes sensitive infrastructure. It needs access control.

Walrus combines decentralized storage with Sui-based access control and encryption. The strongest version of the product is portable memory that agents can use without handing full control to one application.

The bull case is Walrus becoming a default memory layer for AI agents, especially inside the Sui ecosystem and adjacent agent frameworks.

The bear case is limited usage. Agent memory needs integrations, fees, retention and developer adoption. Demos will not be enough

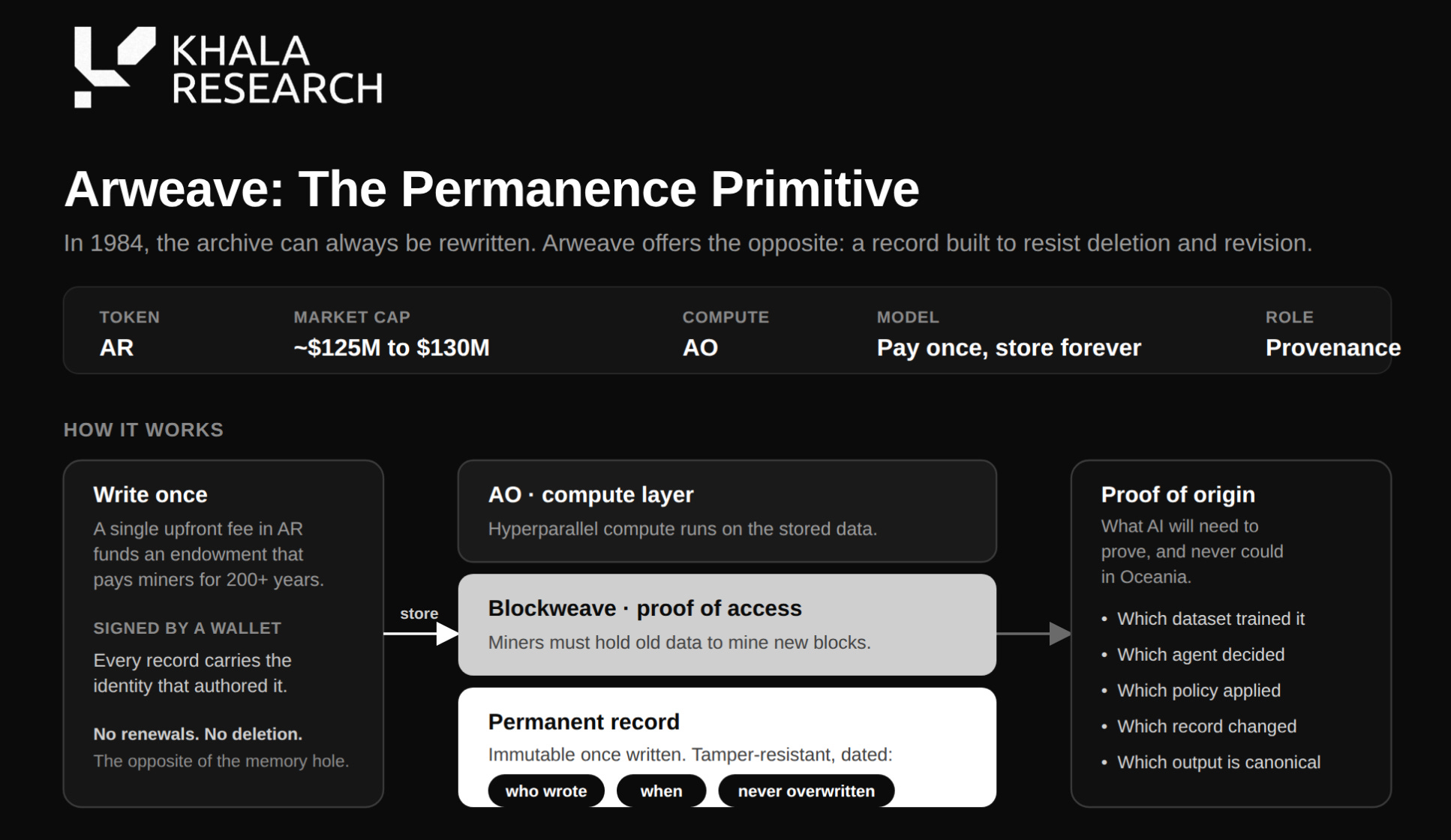

ii) Arweave (AO)

Token: AR

Approx valuation: $125M to $130M market cap

Layer: Permanent storage and AO compute

Memory role: Permanent provenance

Arweave is the permanent-memory trade. Its core value is permanence, which is not right for every type of agent memory but is powerful for provenance

AI creates a large need for proof of origin. Users and developers will need to know which dataset trained a model, which agent made a decision, which policy existed at the time, which record changed and which output is canonical.

In “1984” the archive can always be rewritten. Arweave offers the opposite primitive: a record designed to resist deletion and revision.

AO adds a compute layer, which gives Arweave a stronger agent angle.

The bull case is that AI provenance becomes a major market.

The bear case is that permanent memory is narrow because many agent memories need to be private, editable or forgettable

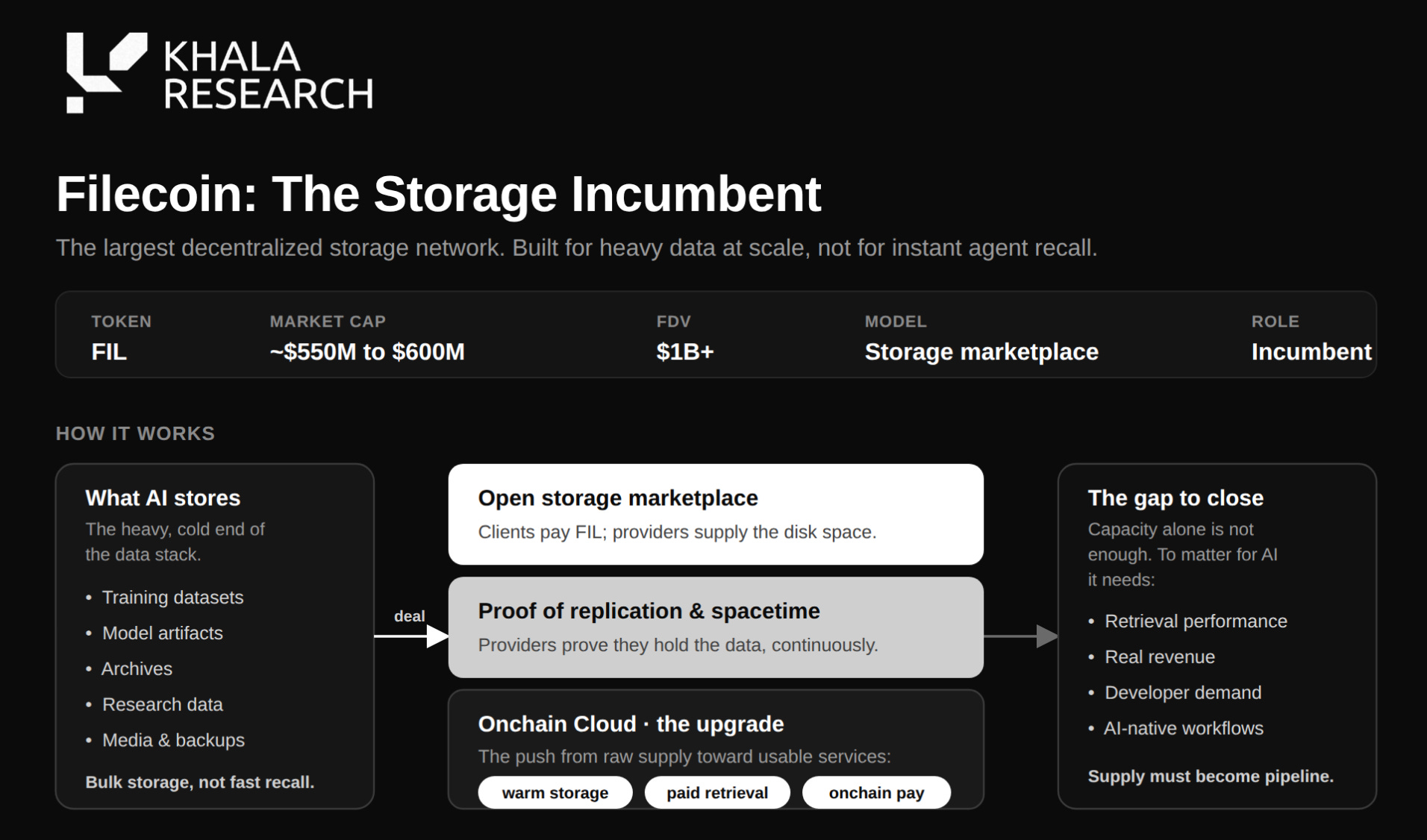

iii) Filecoin

Token: FIL

Approx valuation: $550M to $600M market cap / $1B+ FDV

Layer: Decentralized storage

Memory role: Storage incumbent

Filecoin is the incumbent decentralized storage network. For AI, its strongest angle is large-scale storage: datasets, model artifacts, archives, research data, media and backups. It is more relevant to heavy storage than instant agent recall.

The bull case is that AI data demand grows so large that decentralized storage captures meaningful usage.

The bear case is that storage capacity alone is not enough. The market will want retrieval performance, revenue, developer demand and AI-native workflows.

Filecoin needs to become more than storage supply. It needs to become useful inside real AI data pipelines

iv) Bittensor and Hippius

Tokens: TAO / SN75

Approx valuation: TAO around $2B market cap; Hippius around $15M

Layer: Decentralized AI network and Bittensor storage subnet

Memory role: Bittensor-native memory and storage

Bittensor is a decentralized intelligence market rather than a memory project, which is the core reason Hippius is interesting.

If Bittensor becomes a serious AI economy, it will need internal infrastructure for inference, routing, evaluation, datasets, storage and memory. If you’re want an understanding of its investment history - read out latest report:

Hippius, Subnet 75, is the clearest memory and storage expression inside that ecosystem. It focuses on decentralized storage, cloud infrastructure and persistent memory services for Bittensor.

The investment case is not that Hippius is a standalone category leader in agent memory. The case is that it is a memory and storage layer inside one of crypto AI’s largest networks.

This is different from Walrus. Walrus is a cleaner agent-memory bet. Bittensor and Hippius are an ecosystem-linked bet: if the subnet economy professionalises, storage and memory services become part of the internal AI supply chain.

The bull case is that Bittensor demand grows and subnet-level infrastructure becomes valuable.

The bear case is that subnet valuations remain reflexive, alpha-token methodology is difficult to underwrite, and storage usage inside Bittensor does not become large enough to support the narrative.

7. The memory hierarchy

This is the valuation gap that makes the trade interesting.

HBM suppliers sell physical scarcity.

Crypto memory projects sell programmable memory primitives.

They have different products, revenue models and maturity levels, so the comparison is not like-for-like. The shared direction is that AI systems need more memory and that the market has already rewarded the physical layer more aggressively than the agent-memory layer.

The public market has priced physical memory as infrastructure, while crypto still prices agent memory as optionality. That does not make every token cheap, because most of them still need to prove usage, but it does mean the upside is less capitalised if agent memory becomes a real workflow dependency.

8. Who controls the past controls the agent

The trade comes down to one question: does memory become a workflow dependency?

For equities, the answer is already visible. HBM supply is being reserved, AI customers need more capacity, and data centres need more memory bandwidth, more storage and better interconnects. The market is no longer debating whether memory matters; it’s debating how long the shortage lasts and who captures the most value…

For crypto, the question is still open:

Walrus needs agent integrations

Arweave needs AI provenance usage

Filecoin needs AI storage demand and retrieval relevance

Bittensor and Hippius need storage and memory usage inside the subnet economy

The crypto memory trade only works if agents and users pay for memory directly or indirectly through real workflows… and whether that payment flows back to the token. The age old question of whether the token ACTUALLY accrues value!

AI branding is not enough, storage supply is not enough, and a token attached to a storage narrative is not enough. The winning projects need measurable usage: writes, reads, retrievals, access-control events, paid storage, agent retention and developer adoption.

The most important crypto signal is practical; can a user or enterprise give an agent memory, revoke that memory, move that memory, audit that memory and pay for that memory without depending on one central platform?

If the answer is yes, crypto has a real wedge. If the answer is no, centralized AI platforms become the archive.

9. If there is hope

Orwell’s dystopias were about control. The telescreen watched, the Ministry of Truth rewrote, and the commandments on the barn wall changed while the animals were told the record had always been that way. AI memory creates a similar tension because the most useful agents will be the ones that remember, and the most dangerous memory systems will be the ones that remember without accountability.

The physical memory trade is already large, liquid and well understood. HBM suppliers and memory-linked equities have revenue, supply constraints and strategic customers. Crypto-native memory is smaller, messier and much less proven, but it sits closer to the unresolved question: who owns the memory that makes an agent useful?

Orwell wrote that:

“if there is hope, it lies in the proles.”

In the AI memory trade, the equivalent hope is the part of the stack that has not yet been enclosed. The hardware supercycle is already in the tape and the major platforms already own the user relationship, but the “open memory layer” is still underbuilt and underpriced; that’s the opportunity.

The next decade of AI can inherit the architecture of cloud, where memory stays inside closed platforms, or it can develop an open memory layer where users and agents can carry state across applications with clear permissions and auditability.

One path creates more powerful platforms. The other creates more powerful agents.

Some memory will always be more equal because physics makes fast memory scarce. HBM beside a GPU will always sit higher in the hierarchy than cold storage in an archive. That is a law of infrastructure.

Whether some owners are “more equal than others” is a design choice. If agents become the next users of the internet, memory becomes their past, their permission system, their identity layer and their operating context.

The trade is about who owns that layer.

“All memory is equal, except some memory is more equal than others” - (Sammy, 0x. 2026)

[Inspired by Orwell]

That’s a wrap for issue 182 of Sammy’s Snippets. I hope you enjoyed it.

Please leave me any questions or thoughts here - I will respond to everyone!

If you found this interesting, please consider subscribing to this Substack and following me on X for more related insights.

If you are interested in more formal reporting on Crypto AI and Robotics then Khala is my research product.

Disclaimer: The content of this newsletter is for informational purposes only. Nothing in this newsletter constitutes financial advice or a recommendation to buy or sell any asset. Always do your own research before making any investment decisions.

I hold positions in many of the assets discussed in this newsletter. Valuations are approximate snapshots and move quickly. Verify all market data independently before acting. Quotations from George Orwell’s Animal Farm and Nineteen Eighty-Four are used for commentary and criticism.

Follow me on X | Khala Research