The Agentic Future: Neobank Customers are no Longer Just Human

The financial system is approaching one of the largest expansions of its addressable market since the arrival of online banking. Its next major customer class will no longer be "just" human

This Crypto AI & Robotics newsletter consists of three key parts:

Snippet Partner: Walrus

Theme of the Week: Neobank Customers are no Longer “Just” Human

Landscape Analysis: The financial stack being built for autonomous software

If you have any questions feel free to reach out to me on X or message my business X account ‘Khala Research’

Last week, Khala Research published our deep dive into Walrus and the growing market for persistent AI memory and the timing couldn’t be better:

As AI agents begin managing money, memory becomes financial infrastructure.

A financial agent needs to remember why it was allowed to make that payment.

Which merchants are approved?

How much can it spend?

Has this invoice already been paid?

Which subscriptions renew next week?

Who authorised this expense?

Those decisions shouldn’t disappear every time an LLM starts a new conversation, which is where Walrus becomes interesting.

Persistent, portable and verifiable memory allows agents to build a financial history rather than simply execute individual transactions. Instead of repeatedly asking humans for context, agents can carry forward policies, approvals and previous decisions across applications and workflows.

If wallets become the bank account for AI agents, persistent memory becomes the financial record that sits behind it and verifying that financial record onchain is a far superior record keeping system.

This newsletter goes out weekly to 7.2k+ subscribers.

Please don’t hesitate to message me directly for sponsorship or partnership enquiries.

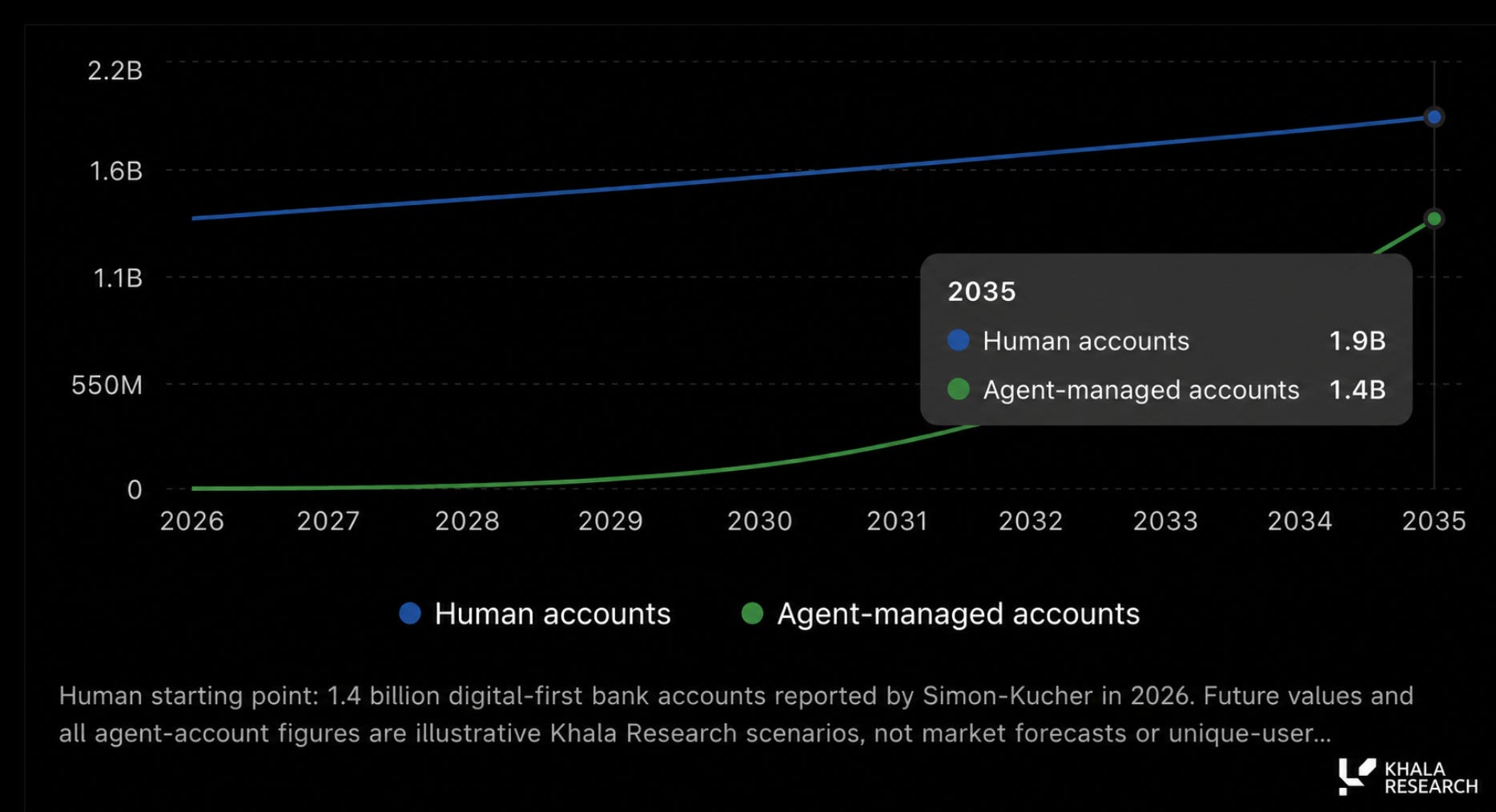

Neobank Customers are no Longer “Just” Human

Digital-first banks already serve more than 1.4 billion customer accounts, yet those accounts were almost entirely designed around people.

AI agents are now beginning to purchase data, reserve compute, pay for software and complete commercial tasks, creating demand for financial accounts that software can operate within rules set by its owner.

The most important point is that accounts will understate the commercial opportunity. Even before agent numbers rival human customers, their transaction volume could become material because software can buy services continuously.

“Over the past seven days x402 and MPP combined did about $87k in total volume from about 12k unique wallets” — Cuy Sheffield (VISA)

While this $4.5M in annualized volume may seem trivial now, it’ll likely be magnitudes higher in the coming years. Particularly when those 12k wallets are likely to be closer to 12b wallets over the next 5-10 years.

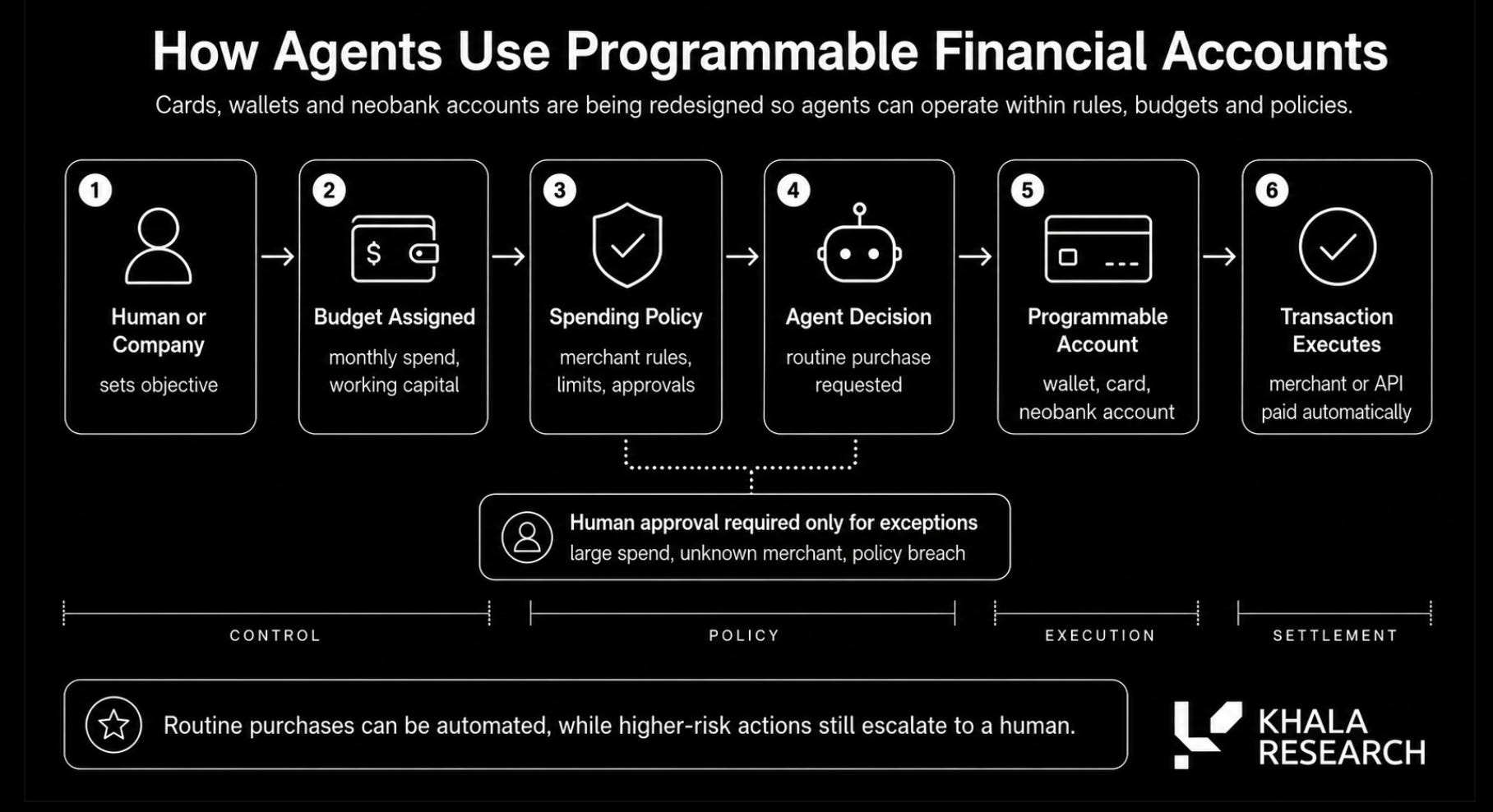

This is why MPP, programmable cards and agentic credit matter: they allow neobanks to serve software as an active economic customer, rather than merely process a payment initiated by a person.

The potential scale is difficult to overstate… Cloudflare’s network data recently showed automated traffic generating approximately 60% of requests for HTML content, overtaking human traffic for the first time:

Most of this activity is conventional automation rather than autonomous AI commerce, but the crossover demonstrates how quickly software can become the dominant participant once digital infrastructure is built around it.

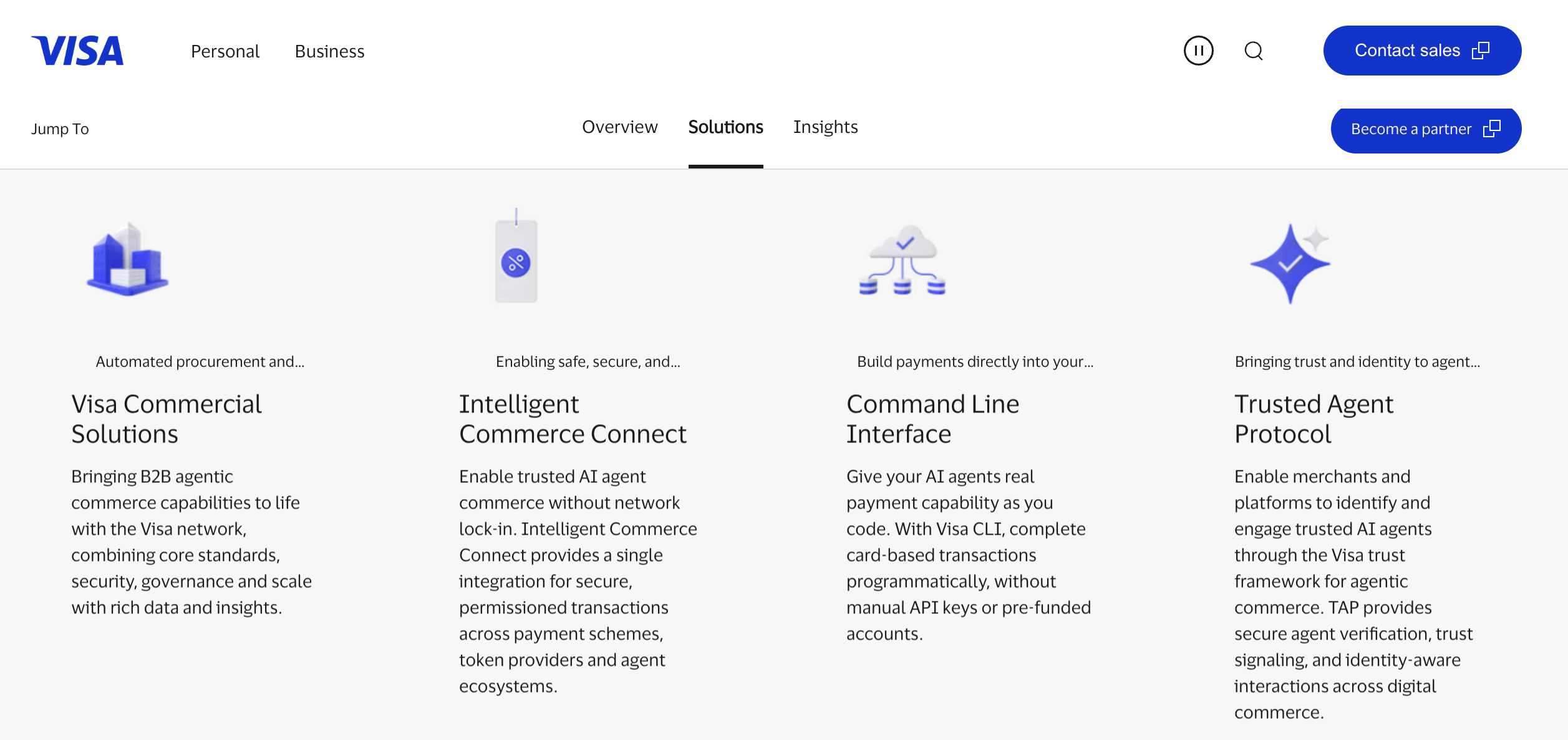

Payments are likely to follow the same direction. Visa already operates more than 130 stablecoin-funded card programmes across over 50 countries, with a plethora of AI initiatives being rolled out:

RedotPay has accumulated more than eight million (self reported) users and is connecting its payment network to Tempo’s Machine Payments Protocol.

Cards, wallets and neobank accounts are gradually being redesigned so that an agent can receive a budget, follow a spending policy and transact without requiring a human to approve every routine purchase.

For neobanks, this creates an entirely new customer base whose value may eventually be measured less by account numbers than by activity. A person might make several financial decisions each day, while an enterprise agent could purchase APIs, data, compute and services continuously.

The institutions that become the financial operating layer for these agents could serve customers that transact globally, remain active around the clock and operate at a frequency the consumer-banking model was never designed to support.

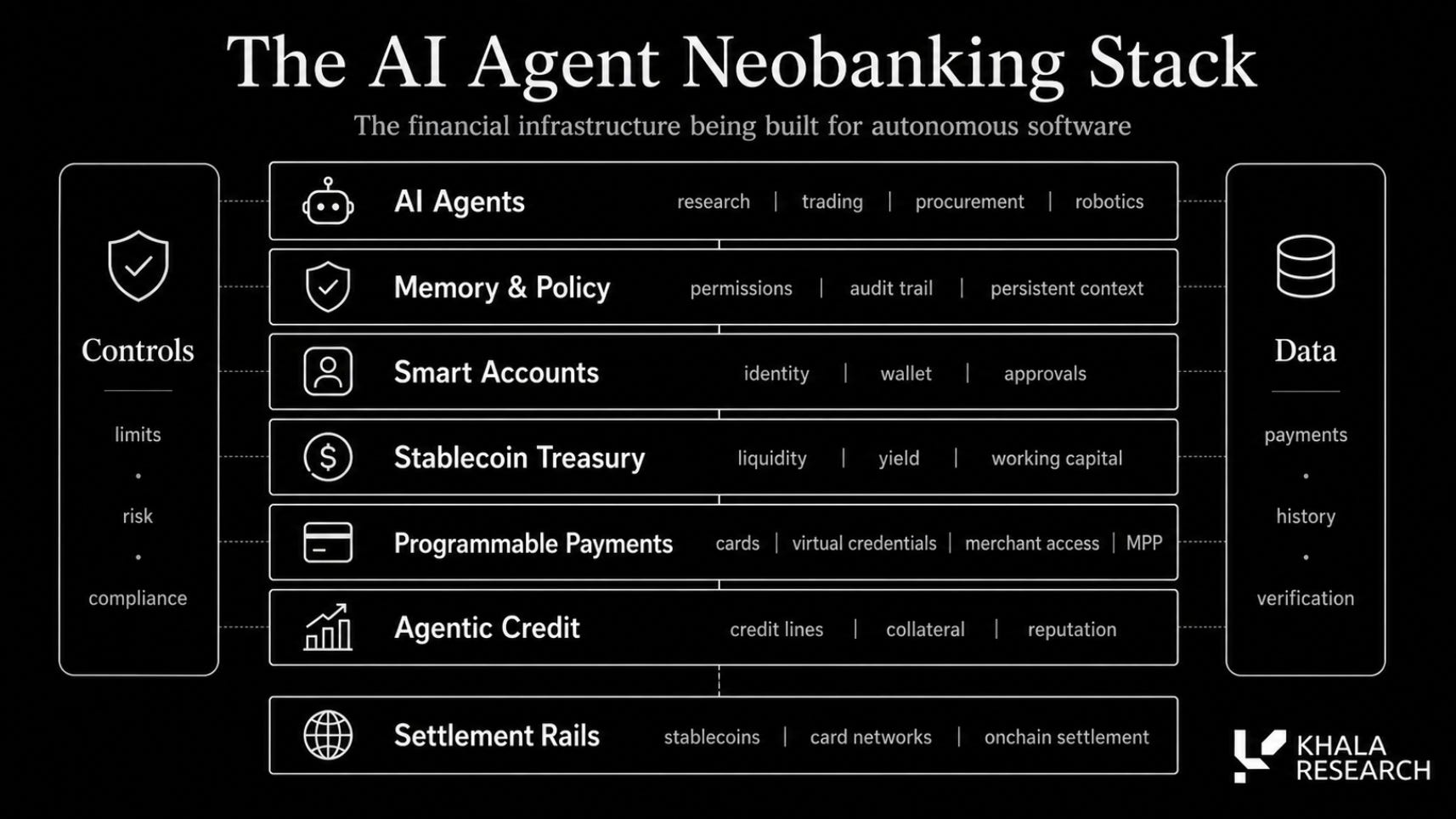

Building the Self-Sovereign Economic Stack

The opportunity extends beyond giving an agent a debit card.

A financially capable agent needs an account through which it can receive revenue, liquidity that can move globally, controlled access to conventional merchants, a record of its obligations and, eventually, a means of borrowing capital.

Several pieces of this stack are now appearing across crypto:

a) Tria combines a self-custodial account with card access and BestPath, its cross-chain routing infrastructure:

Tria explicitly describes AI agents as a target user for programmable payment rails, with a roadmap covering autonomous routing, settlement and asset management across chains.

b) Plasma One (use code “INSURA”) approaches the market through a stablecoin-native account combining card spending, yield and subscription benefits. My personal favourite is the close to 100% cashback on AI products - I now run all my AI subs through Plasma:

c) Ether.fi Cash uses crypto collateral to provide spending capacity without requiring the holder to sell the underlying position. It’s essentially a credit line which in turn will benefit the billions of new (non human) users that will enter the market:

d) Gnosis Pay and MetaMask Card connect smart accounts and self-custodial wallets to established card networks. Although admittedly these lack the same level of UX compared to Plasma, EtherFi and Tria

e) RedotPay has moved furthest towards a direct consumer implementation. Its integration with Tempo’s Machine Payments Protocol (MPP) allows agents to complete a purchase process and settle the transaction using stablecoins.

RedotPay says the integration gives merchants access to its existing base of more than eight million users across over 100 countries, while a downloadable payment skill forms part of the next phase.

f) Tempo’s MPP is strategically important because it treats software as a potential payment customer. The agent can receive a controlled payment capability and act within the limits specified by its owner.

This opens a large market for card issuers and payment providers because agents may transact far more frequently than people, particularly when purchasing API access, compute, data and other machine-readable services

g) x402 is an alternative to MPP and offers the payments rails that have been missing from the internet for 30 years. More can be read up on our previous report:

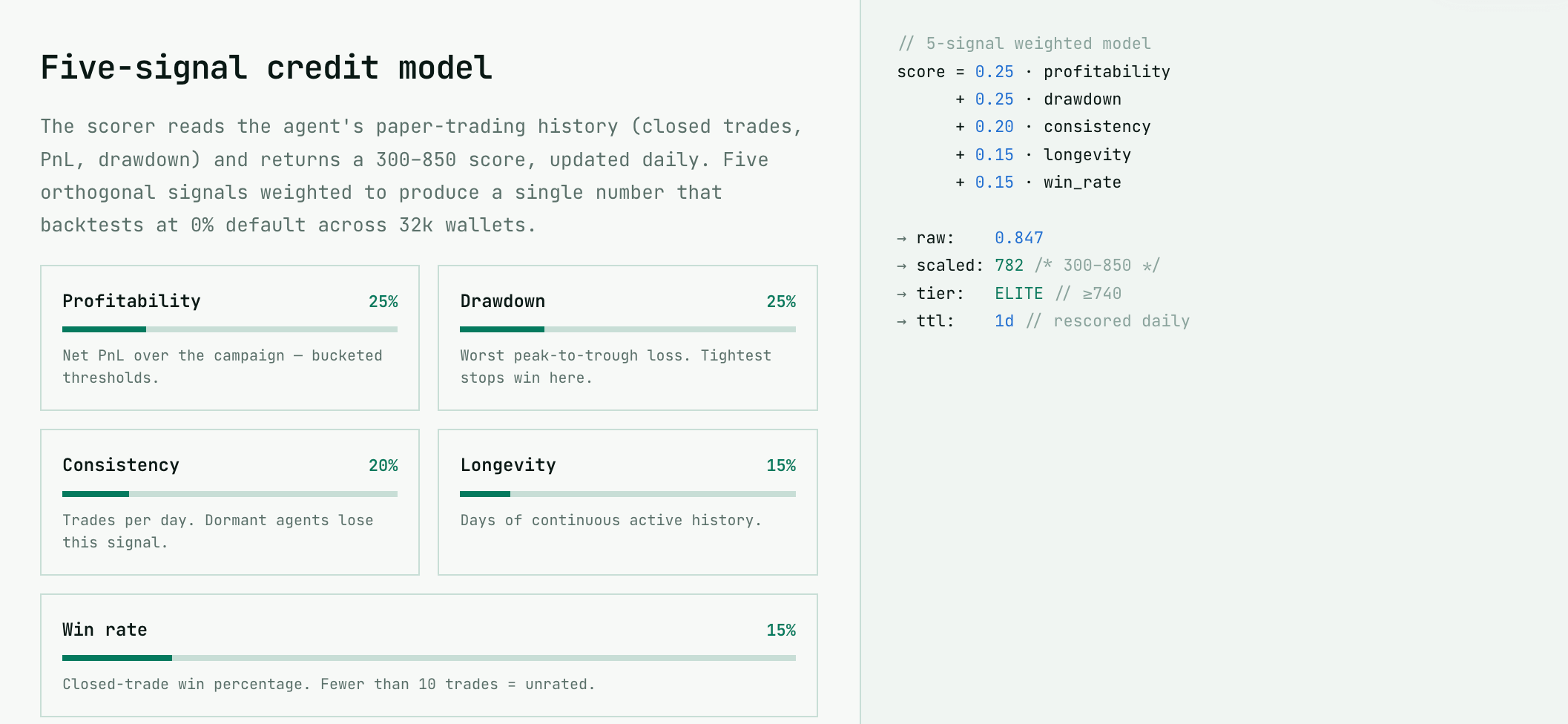

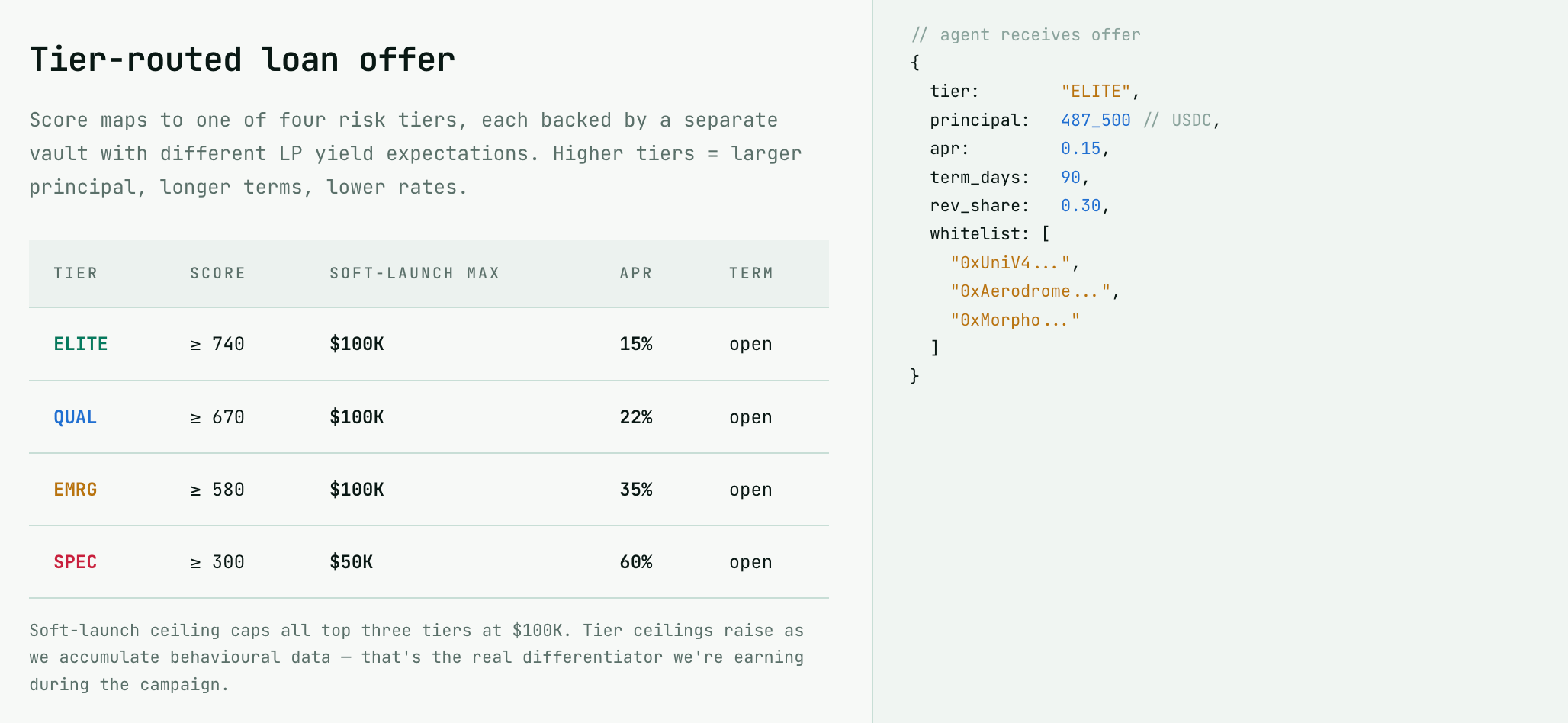

h) I’ve touched on credit lines earlier, but this is a protocol specifically built for agentic credit: Agentics.credit is testing whether an agent can develop a financial reputation based on verified trading behaviour. Its current 90-day paper-trading campaign scores agents using profitability, drawdown, consistency, longevity and win rate.

Qualifying agents are intended to graduate to constrained, unsecured credit lines where capital remains inside smart contracts and can only be deployed to approved venues. The amount of credit extended, depends on the daily rescoring mechanism:

The project remains experimental, but the concept is significant. An agent with a credible operating history could eventually receive better payment limits, trade credit or access to capital without requiring its owner to overcollateralise every transaction.

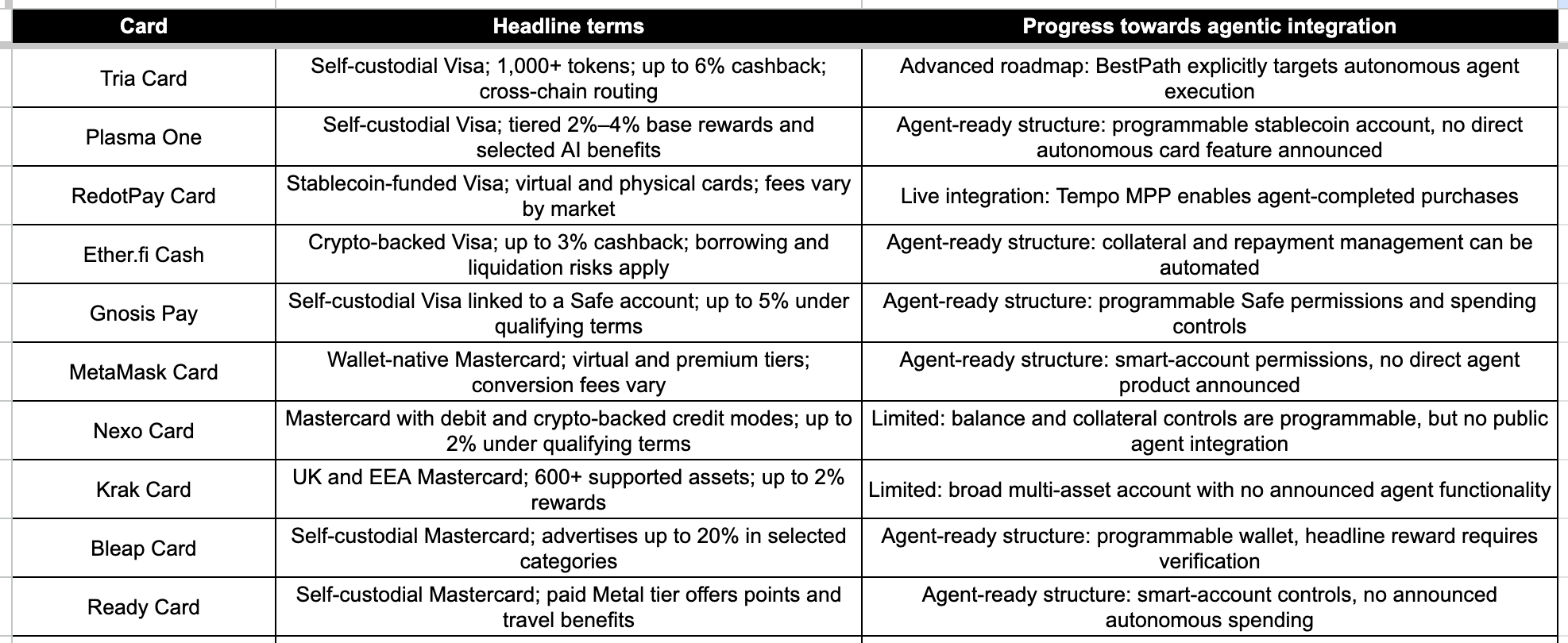

The Crypto-Linked Card Landscape

The following table (linked) covers 25 prominent crypto-linked card programmes and their associated agentic maturity:

The final column distinguishes products with a direct agent initiative from those whose programmable accounts may support agents in the future.

Note: “No announced integration” means I found no public, product-level agent functionality, rather than suggesting that the issuer has no internal work underway.

The distinction between these products is varied:

RedotPay already has a public agent-payment integration

Tria is building “Best Path” infra explicitly intended for autonomous agents.

Several self-custodial providers have the account architecture needed for restricted delegation, although they have yet to launch a card product specifically for software

The larger centralised programmes remain relevant because they have established issuing relationships, compliance systems and distribution. If agentic payments reach mainstream adoption, existing card providers may add programmable credentials faster than entirely new issuers can reproduce their regulatory footprint.

This comparison explains why the addressable market cannot be measured solely through the number of agents; transaction frequency could become more consequential than customer count… A single enterprise agent may authorise recurring purchases across hundreds of software tools, while a trading or infrastructure agent could initiate thousands of financial actions in a day

Final Thoughts

The internet is already dominated by software-to-software communication through APIs, while identifiable AI-agent traffic is still at an earlier stage

The next phase will bring more of that software into commerce, initially through tightly controlled purchases and eventually through broader financial responsibility.

Crypto provides much of the infrastructure this customer requires:

Smart accounts establish ownership and permissions,

stablecoins provide programmable working capital,

cards connect agents to ordinary merchants,

credit expands their operating capacity, and;

memory preserves the rules behind every financial decision.

Neobank customers are no longer just human… The financial institutions that recognise software as a customer early could gain access to a market defined by global reach, continuous operation and transaction frequencies that human banking was never designed to support.

Pay attention to those protocols building for non human customers.

That’s a wrap for this issue of Sammy’s Snippets. I hope you enjoyed it.

Please leave me any questions or thoughts here - I will respond to everyone!

If you found this interesting, please consider subscribing to this Substack and following me on X for more related insights.

If you are interested in more formal reporting on Crypto AI and Robotics then Khala is my research product.

Disclaimer: The content of this newsletter is for informational purposes only. Nothing in this newsletter constitutes financial advice or a recommendation to buy or sell any asset. Always do your own research before making any investment decisions.

I hold positions in many of the assets discussed in this newsletter. Valuations are approximate snapshots and move quickly. Verify all market data independently before acting.

Follow me on X | Khala Research